Identification of AIBSNLPWA Under Pensioners Portal Copy of order

==========================================================

CONTACT NUMBERS:

REGISTRATION CERTIFICATE: regn-certificate-with-translation.pdf

CONSTITUTION: constitution.pdf

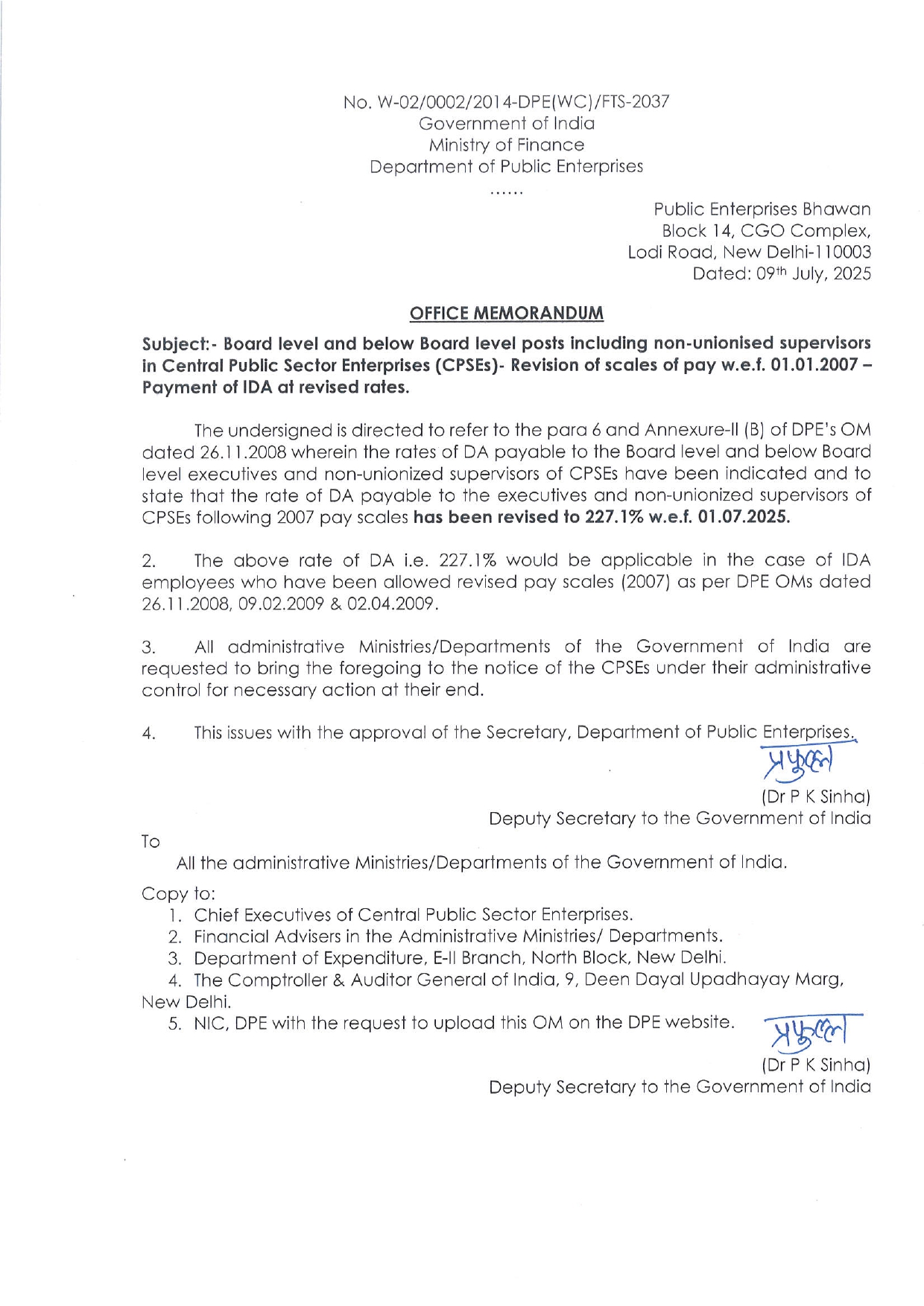

A Rates from 2007: rate-of-ida-from-2007-to-2024.pdf

FOR ONLINE REMITTANCE TO CHQ :

Name

of recipient: AIBSNLPWA (CHQ), SB A/c No 67100927818,

IFSC No. SBIN0002239

After remittance of any amount, please intimate the details to Treasurer :

Shri T S Vittoban, Block-A, Flat- D4, Air View Apartments, (Near

City Union Bank),

Contact Numbers: Please see list of Office Bearers

Latest News

The matters were listed today (29-07-2025) before HMJ Navin Chawla and HMJ Shalinder Kaur.

The Union of India started arguing the matter.

The Court asked Mr Ghose about the issue and he explained that in terms of Rule 37 Sub Rule 8A of the CCS Pension Rules, the absorbee pensioners were promised parity in the matter of pension with central government pensioners. He further told the Court about the recent Kerala HC judgment where the Court has reaffirmed this position.

The Counsel for Union of India essentially referred to a chart submitted by them as part of the written submissions to demonstrate how BSNL absorbee pensioners are getting more pension than Central Government pensioners. He also stated that the Union will be filing an SLP against the judgment of the Kerala High Court.

The Court posted the matter on 19th August at 3:30 PM for further arguments.

Organized by: Forum of Civil Pensioners’ Associations - Despite widespread rains in several parts of the country, the Human Chain protest held today, 25th July 2025, was a resounding success across India. This coordinated action was undertaken to oppose the draconian Validation Clause in the amended Pension Rules, which seeks to deny pension revision benefits to past pensioners.

Reports poured in from all directions—rural towns, state capitals, metro cities—reflecting one thing clearly: Today we saw the first link in a long chain of struggle. This protest was only the first phase. The chain of resistance has formed. Let us strengthen it link by link, until justice is restored. This is only the beginning of a long, sustained campaign for:

The abolition of the Validation Clause

Pension revision with full parity

Timely constitution of the 8th Central Pay Commission

We have made our stand clear. The Government may ignore us temporarily. The Government may refuse to correct a wrong decision. But we will not give up. We will resist.

The CHQ of AIBSNLPWA congratulates and thanks every District and Circle unit, every partner organization, and every individual pensioner who made today’s protest a nationwide success.

The Circle Conference of AIBSNLPWA Orissa Circle was held on 24th July 2025 at BSNL Conference Hall, Bhubaneswar, presided over by Com. Ramesh Mohanty.

Circle Secretary Com. B.N. Behera 's report and ; audited accounts also were approved.

Com. V. Vara Prasad, GS, and Com. J.K. Tripathy, VP (CHQ) addressed the gathering.

Senior BSNL officers — Shri D.K. Behera (CGM), Shri B.K. Behera (PGM, Circle Office), and Shri I.G. Soren (PGM, BBS) — participated and spoke.

97 delegates attended. The following were elected unanimously:

President: B.D. Panda

Secretary: B.N. Behera

Treasurer: S.C. Satpathi

District Conference of Mangalore was held on 08-07-2025. Com Jaya Shankar Circle Secretary Participated as Chief Guest. About 300 members attended the conference. The following office bearers were elected unanimously.

President : Com H Ramakrishna

Secretary Com K Chandra Mohan

Treasurer : Hema U Pai

The District Conference of Karnal (Haryana) was held on 6th July 2025 at Karnal. Com. Trilok Chand, Com. Balkrishan Panwar, and Com. Hansraj were unanimously elected as President, District Secretary, and Treasurer, respectively. Com. J.S. Malik, Circle Secretary, and Com. J.S. Dahiya, Organising Secretary (CHQ), graced the occasion and addressed the delegates.

A courtesy meeting was held with Com. Shiva Gopal Mishra, President NCCPA, during his visit to Vijayawada on 2nd July 2025, where Com. R.S.N. Murty, Com. K. Bhaskara Rao, and Com. V. Vara Prasad discussed issues of mutual concern, including the impact of the Validation Act and the demand for inclusion of BSNL pension revision under the 8th CPC Terms of Reference. Com. Ch. Sankara Rao, General Secretary, SCRMU, was also present.