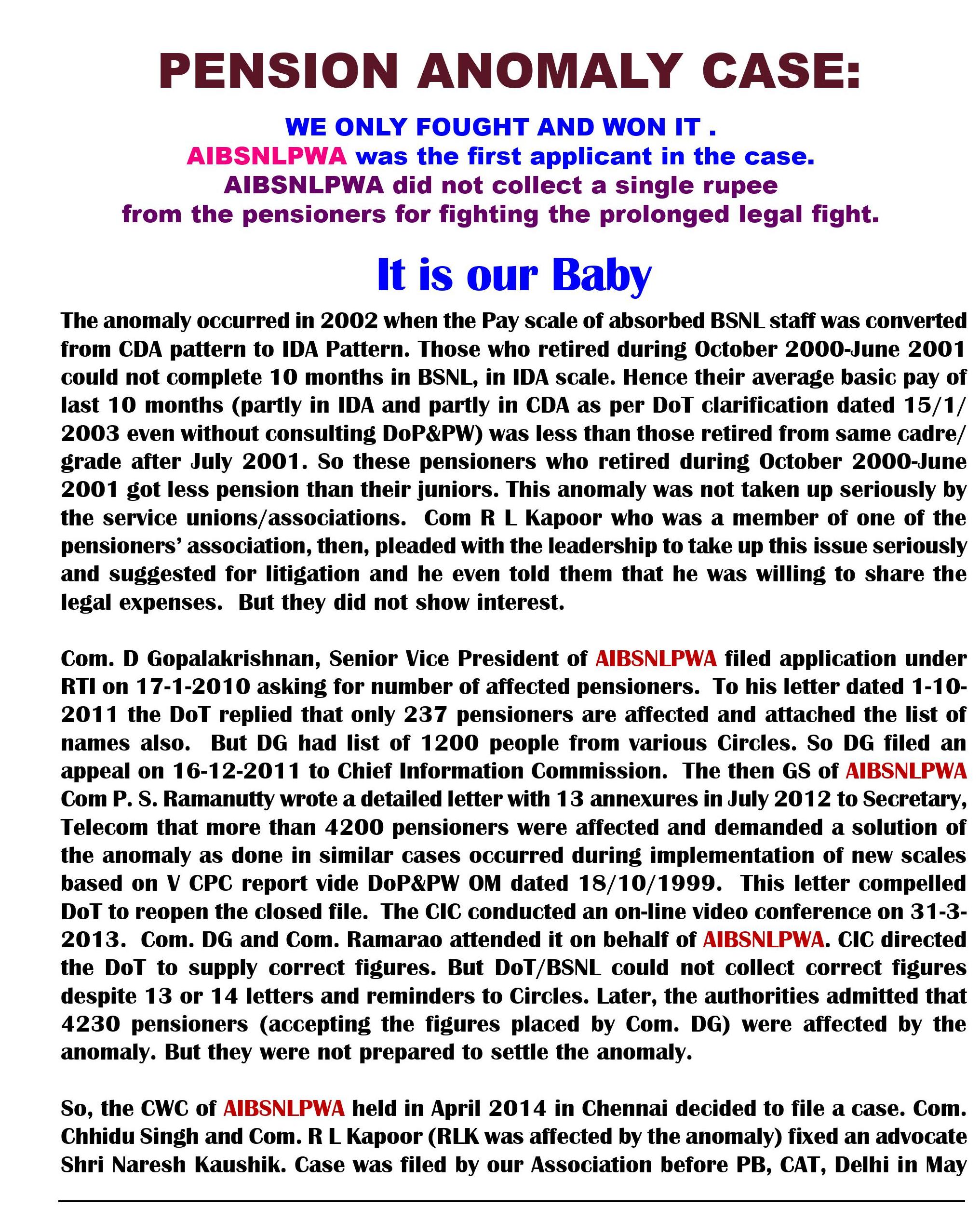

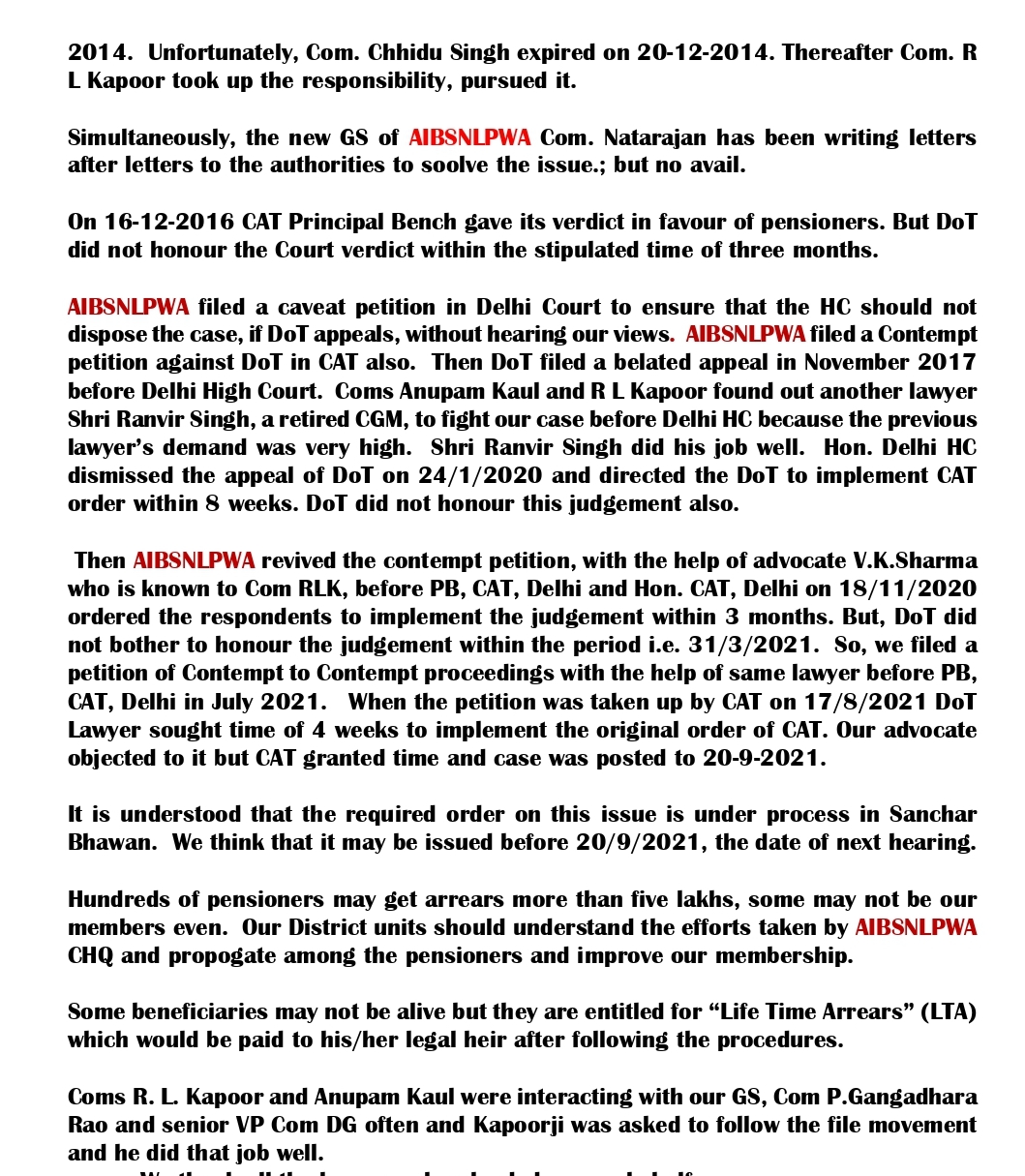

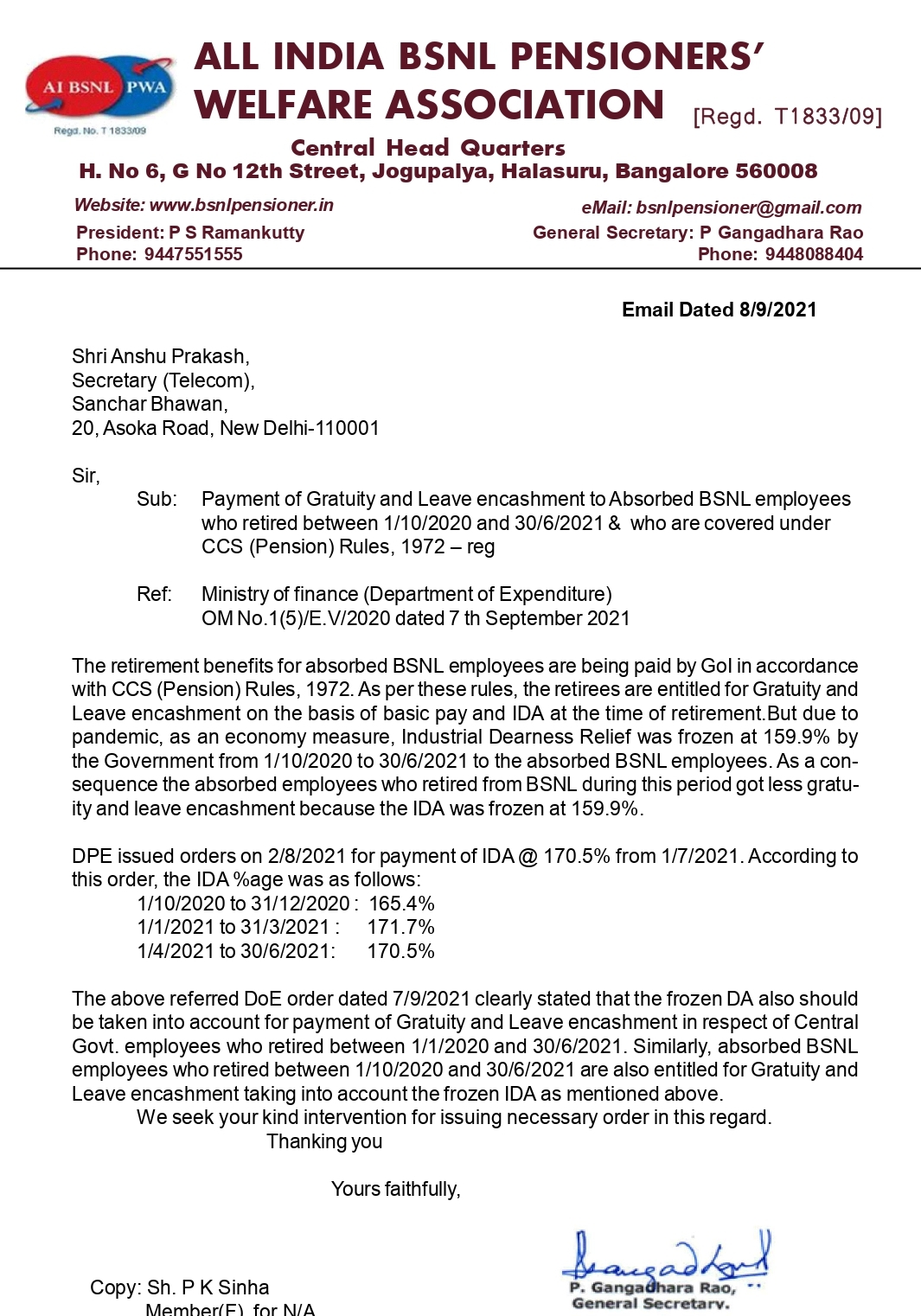

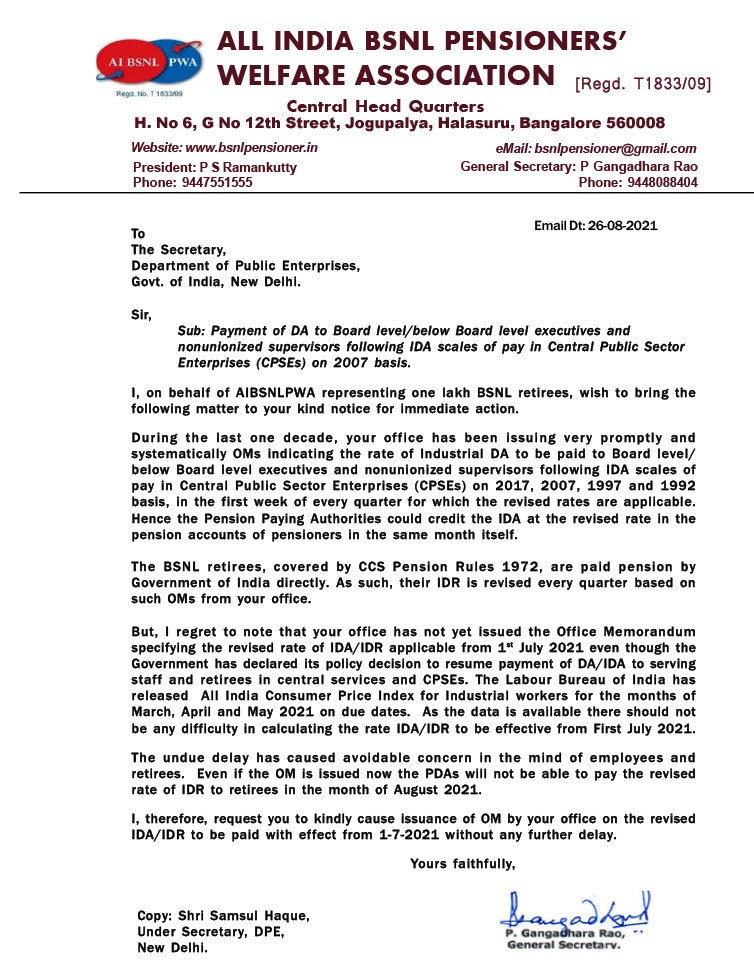

Archives-News

Please click here to read the E Journal No 14 for September-October 2021e-journal-sept-oct-2021.pdf

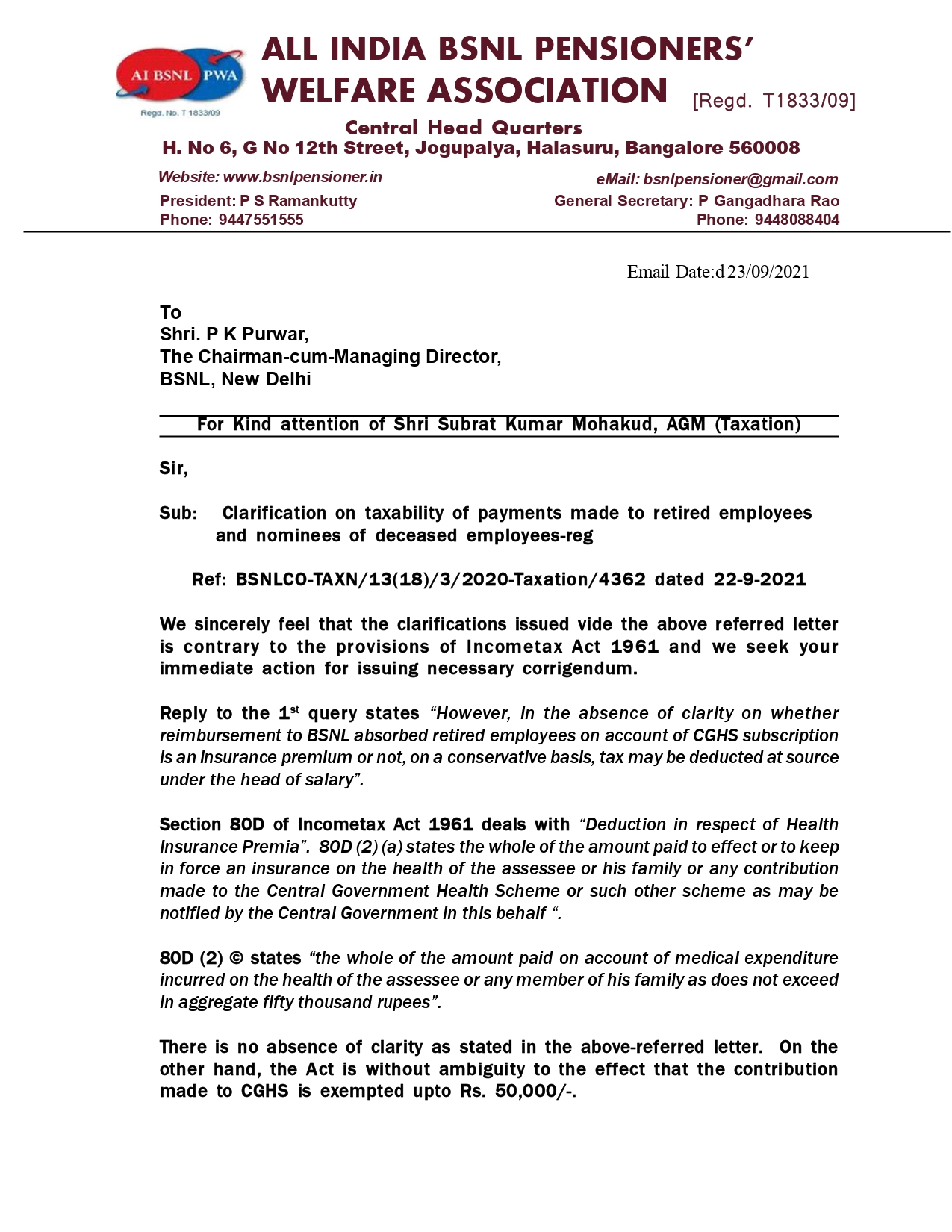

A STRANGE CLARIFICATION BY BSNL ON

A STRANGE CLARIFICATION BY BSNL ON

TAXATION ON CGHS and GRATUITY.

BSNL CO Letter No. BSNLCO-TAXN/13(18)/3/2020-TAXATION/4362

Dated:-22-09-2021

To

1) The Chief General Managers and IFAs, All BSNL Circles/Units.

2) Sr.GM (CA/ERP-FICO/HCM), Corporate Office

3) GM (EF/ R&P), Corporate Office

Sub.:- Clarification on taxability of payments made to retired employees and

nominees of deceased employees-reg.

The undersigned is directed to intimate that, this office is receiving queries from the various circle on the subject mentioned above. In this connection the para wise replies to the queries raised by circles are as follows:-

Query: Whether reimbursement of CGHS subscription to BSNL absorbed retired employees is to be treated as income of the retired employee? And, if the answer is in affirmative, the head under which it is chargeable.

Reply: As per the proviso to section 17(2) of the Income Tax Act,1961 any reimbursement by the employer in respect of any insurance premium paid by the employee to effect an insurance on his health or the health of his family under any approved scheme by Central Govt. or IRDA is a tax free perquisite. However, in the absence of clarity on whether reimbursement to BSNL absorbed retired employees on account of CGHS subscription is an insurance premium or not, on a conservative basis, tax may be deducted at source under the head of salary.

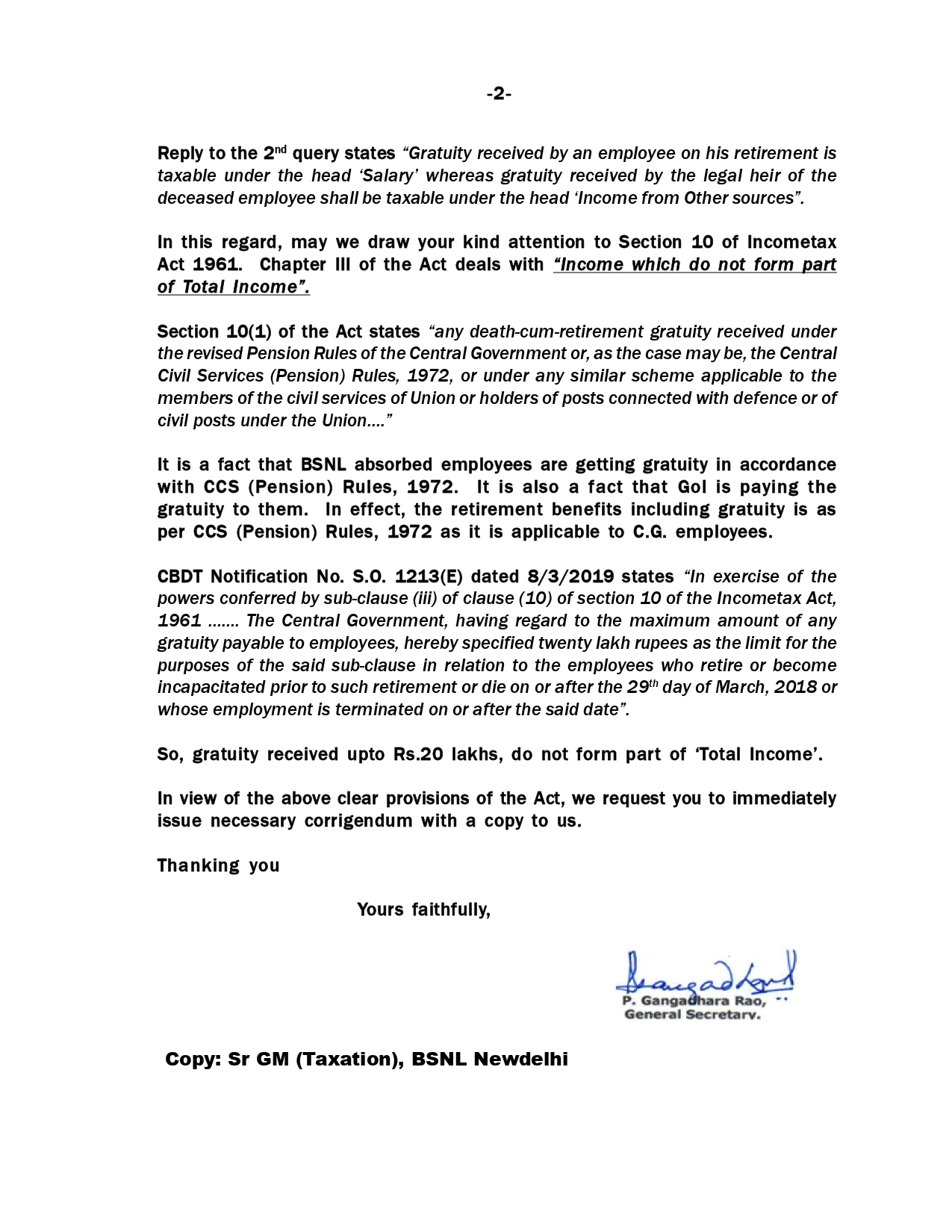

Query: Gratuity/Leave encashment payable to Nominee/Legal Heirs of BSNL employee on death while in employment is to be shown as Income of the employee or legal heirs? And the head under which it is chargeable.

Reply:

(i) Gratuity is a payment made by Employer to an Employee in appreciation of the past services rendered by the employee. Gratuity can either be received by:-

a) The employee himself at the time of retirement.

b) The legal heir on the event of the death of the employee.

Gratuity received by an employee on his retirement is taxable under the head “Salary”Whereas gratuity received by the legal heir of the deceased employee shall be taxable under the head “Income From Other sources”.

As per circular No. 573 dated 21.08.1990, Gratuity payment to a widow or other legal heirs of any employee who dies in active service shall be exempt from income tax.

(ii) Leave salary paid to the legal heir of deceased employee is not taxable as salary.

[Letter No. F.35/1/65-IT(B), dated 5/11/1965 ].

Further, leave salary by a legal heir of the Government employee who died in harness is not taxable in the hands of the recipient[Circulars No.309, dated 3/7/1981].

Query: Medical Reimbursement to the spouse/dependents of the deceased employee is taxable under which head of Income tax.

Reply: As per section 56(1) of the Income tax act, Income of every kind which is not to be excluded from the total income under this Act shall be chargeable to income-tax under the head “Income from other sources”, if it is not chargeable to income-tax under any of the heads specified in section 14, in other words, the following conditions must be satisfied before an income can be taxed under the head of “Income from other source” :-

(i) there must be an income.

(ii) such income is not exempt under the provision of the income tax act.

(iii) such income is not chargeable to tax under any first four heads viz., “Income from

Salary”, “Income from House Property”, “Profit and Gains of Business and Profession”,and “Income from Capital Gains”.

Income from other source is, therefore, a residuary head of income.

In view of the above medical reimbursement to the spouse/dependents of the deceased employee is taxable under the head of “Income from other source” of Income tax.

It is requested to kindly go through the above instructions and contents of the same may be brought to the notice of all concerned for their information and further necessary action.

This issues with the approval of Sr. GM (Taxation).

Please click here to see the Om from DoP&PW on the subject: lc-2021.pdf

Please4 cilck here to read a write up by P S Ramankutty; salute-the-martyrs.pdf

Please click here to see a Ready Recknor Excel format.anomaly-arrears..-9-tables.xls

There are Nine Tables. One for each month From October 2000 to June 2001

Go to the Table for the month in which you retired.

On the top of each TABLE, you have to enter two figures:

1. revised basic pension granted in 2002 for Non Executives and

in 2009 for the Executives....in place of 5000

2. the basic pension to be revised as per CAT order, in place of 6000

Please click here to see a write up on PENSION ANOMALYDOWN THE MEMORY LANE

THE CONVERSION TABLES used in 2002/2009: conversion-tables-used-in-2002-and-2009.pdf

OUR PENSION REVISION CASE WAS TAKEN UP BY PRINCIPAL BENCH OF CAT YESTERDAY, 5-8-2021.

OUR LAWYER POINTED OUT THAT BSNL HAS NOT YET FILED ITS REPLY DESPITE THREE CHANCES WERE GIVEN. AS SUCH RIGHT TO REPLY SHOULD BE CLOSED AND ARGUEMENTS SHOULD BE STARTED. HOWEVER THE COURT GRANTED ONE WEEKS TIME TO BSNL TO FILE ITS REPLY.

REPLY FROM RESPONDENTS WAS TAKEN ON RECORD.

NOW THE CASE IS POSTED TO 10-9-2021.

......

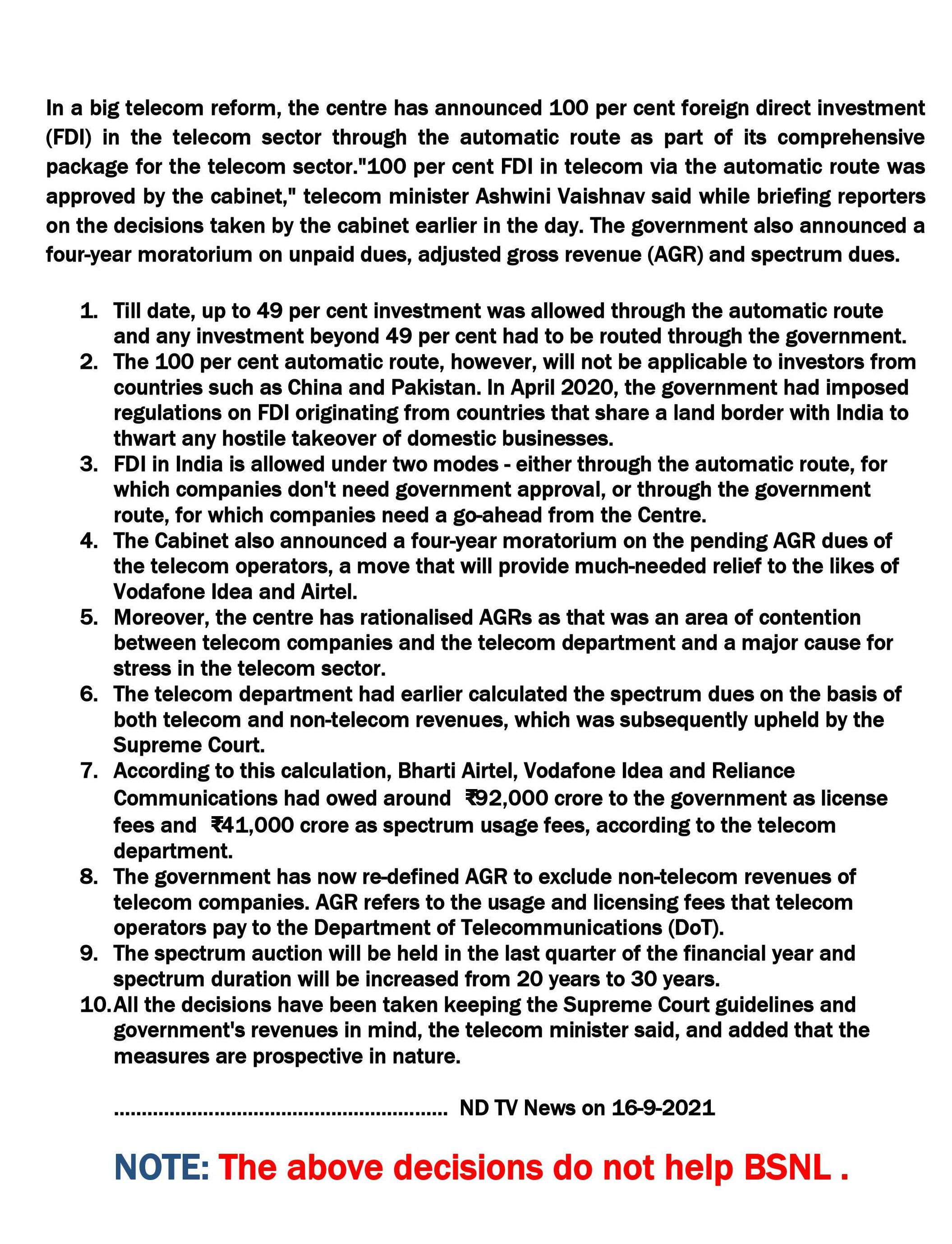

The DPE Order dated 2-8-2021: Please click here ida-unfreeze.pdf

Calculation as per DPE method-new

March 2021 - 119.6 × 2.88 = 344.45 (119.6 is Index in new Series)

April 2021 - 120.1 × 2.88 = 345.89 (345.89 is Index in earlier Series)

May 2021 - 120.6 × 2.88 = 347.33

Total of 3 Months = 1037.67

Average of 3 months = 345.89

Increase over Link Point of 126.33: 345.89 - 126.33 =219.56

219.56 × 100 = 21956

21956 ÷ 126.33 = 173.8

Therefore we are entitled to 173.8 % IDA from 1st July, 2021 for which orders are to be issued. In the same way June index is 121.7 (2016=100) and if we convert it to 2001= 100 series it comes to 350.50

Earlier 2001 = 100 series Index figures were always in round figures. But while converting 2016 = 100 figures to 2001=100 with convertion factor of 2.88 DPE is taking upto two decimal Points. (Please see work sheet of DPE Orders)

[Above input is from Com. V V S Murthy, former AGS at Hyderabad.]

Earlier, the All India Consumer Price Index for Industrial Workers, on which our IDA rate is fixed, was based on a Series with 2001 point = 100. Now a new Series with base year 2016=100 point is adopted. And the AICP Index is published as per new Series. For those who continue in 2007 Pay Scales, the new Index in new Series has to be converted in to old Series by multiplying with a factor of 2.88. That is why 119.6 (new Series) is converted in to 344.45 (earlier Series.) For those CPSE employees who got pay revision from 1-1-2017 the IDA is increased from 18.4% to 23.2%. ...PSR

CDA released for the CPSE Employees following CDA pattern. Some 69 CPSEs are following CDA pattern for their serving staff. The attached order is applicable for them

Click here to see the DPE order: ej1303.pdf

Department of Expenditure, Ministry of Finance has issued orders on 20-7-2021 releasing the CDA from 1-7-2021.

Please click here to see the order ej1302.pdf