Archives-News

DPE issued orders for revised IDA rates @ 201.2% due from 01-01-2023 in respect of Pay scales of 01-01-2007.

Web portal for providing various online services to retired employees

this service is to be implemented on pan-india level by ITPC Circle.

BSNL retired employees’ portal can be accessed on

https://pensioners.bsnl.co.in/portal/ .

BSNL Letter letter-regarding-bsnl-retired-employees-portal-26.12.2022-1.pdf

Letter addressed to Secretary DOPT for grant of notional increment on completion of 12 months for Pensionary benefits

KARNAL

ALLEPPY

SANGAREDDY

KARWAR

CHIKAMAGALUR

DAVANGERE

MANGALORE

KOTKAPURA - PUNJAB

HUBBALI -DHARWAD

TUMAKURU

MYSORE

BIDAR

MUMBAI PRABHADEVI EXCHANGE DADAR

UDAIPUR

OOTY - NILGIRIS

THANJAVUR

LUCKNOW

RANCHI

BHATINDA

JALANDHAR

BOKARO

SHAJAHANPUR

JAMSHEDPUR

FEROZPUR

BATALA

PATHANKOT

KHOZIKODE

CUTTACK

ERNAKULAM

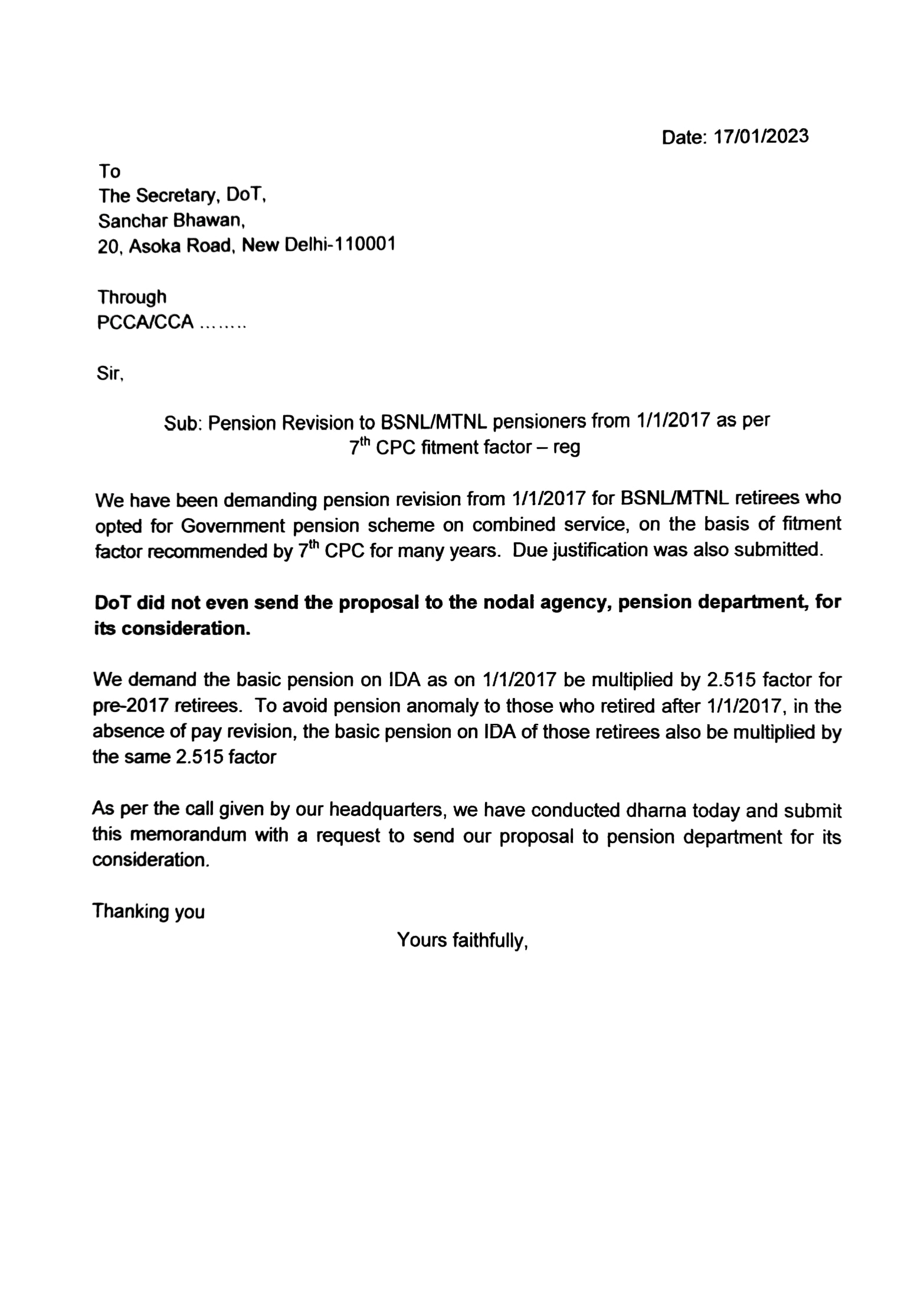

As per call of CHQ to observe call attention day on 19-12-2022 demanding pension revision with 7th CPC fitment benefit , jointly in association with 5 other BSNL/MTNL pensioners associations, all our members have participated in very good number all over the country with great enthusiasm and commitment by holding demonstrations. It is marked with speeches by our CHQ/Circle /District office-bearers, leaders at their respective places. The call was successfully implemented by our units in all circles/branches at CCA/SSA/Local headquarters . We congratulate all our units for this grand success of the program and it is evident and we are sure that our next program of agitations would be done with much more success which will surely compel the DOT to take positive decisions on pension revision as per our justified demand.

Click here link for some of the glimpses : :https://photos.app.goo.gl/WVnkxjbMqkFQDLVU8

FLOWER BAZAR CHENNAI

BERHAMPUR

DHARMASALA

DELHI

HYDERABAD

FARUKABAD

AHMEDNAGAR

BHANDARA

LATUR

SHOLAPUR

GUNTUR

TIRUCHI

THOOTHUKUDI

VELLORE

MADURAI

CHENNAI

ARA

AGRA

SRIGANGANAGAR

SAMBALPUR

MATHURA - UP WEST

CHAPRA

MEERUT

ELURU

SURENDRANAGAR

AHMEDABAD

BHAVNAGAR

KOLLAM

MALLAPURAM

GHAZIABAD

BAREILLY

ETAH

UDAIPUR

TRISSUR

KOTTAYAM

CHANDIGARH

PATIALA

LUDHIANA

PRAYAGRAJ

MOTIHARI

SASARAM

PATNA

MUZAFFARPUR

JAIPUR

KHAMMAM

JABALPUR

GHORAKPUR

OSMANABAD

BHUBANESWAR

HINDUPUR

WARANGAL

SALEM EAST & WEST

CHANDRAPUR

NIZAMABAD

AKOLA

RAJAHMUNDRY

PRATAPGARH

BHARATPUR

SATARA

ANANTAPUR

SITAPUR

KATIHAR

KHOZIKODE

PALAKKAD

VIJAYAPUR

TIRUPATI

KURNOOL

MAHABUBNAGAR

GWALIOR

SAHARANPUR

VIZIANAGARAM

VIJAYAWADA

BANGALORE

NALGONDA

TIRUVALLA (KERALA)

ADILABAD

SRIKAKULAM

VISAKHAPATNAM

ONGOLE

NELLORE

TRIVANDRUM

Andhra Circle Conference was held on 04-12-2022 at Visakhaptnam at Same venue of AIC. Com PSR , DG, PGR, TSV and other CHQ office bearers from AP have addressed.

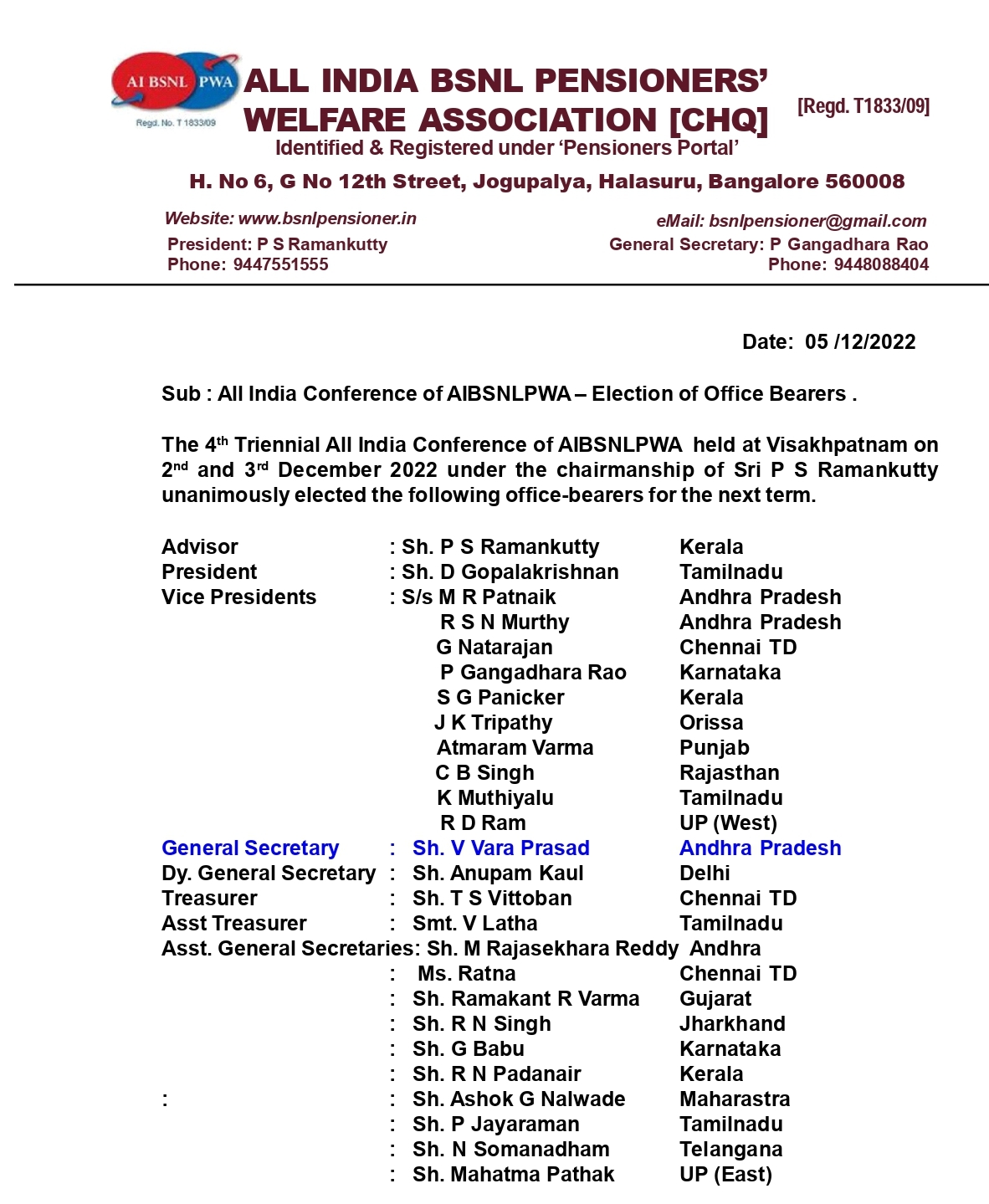

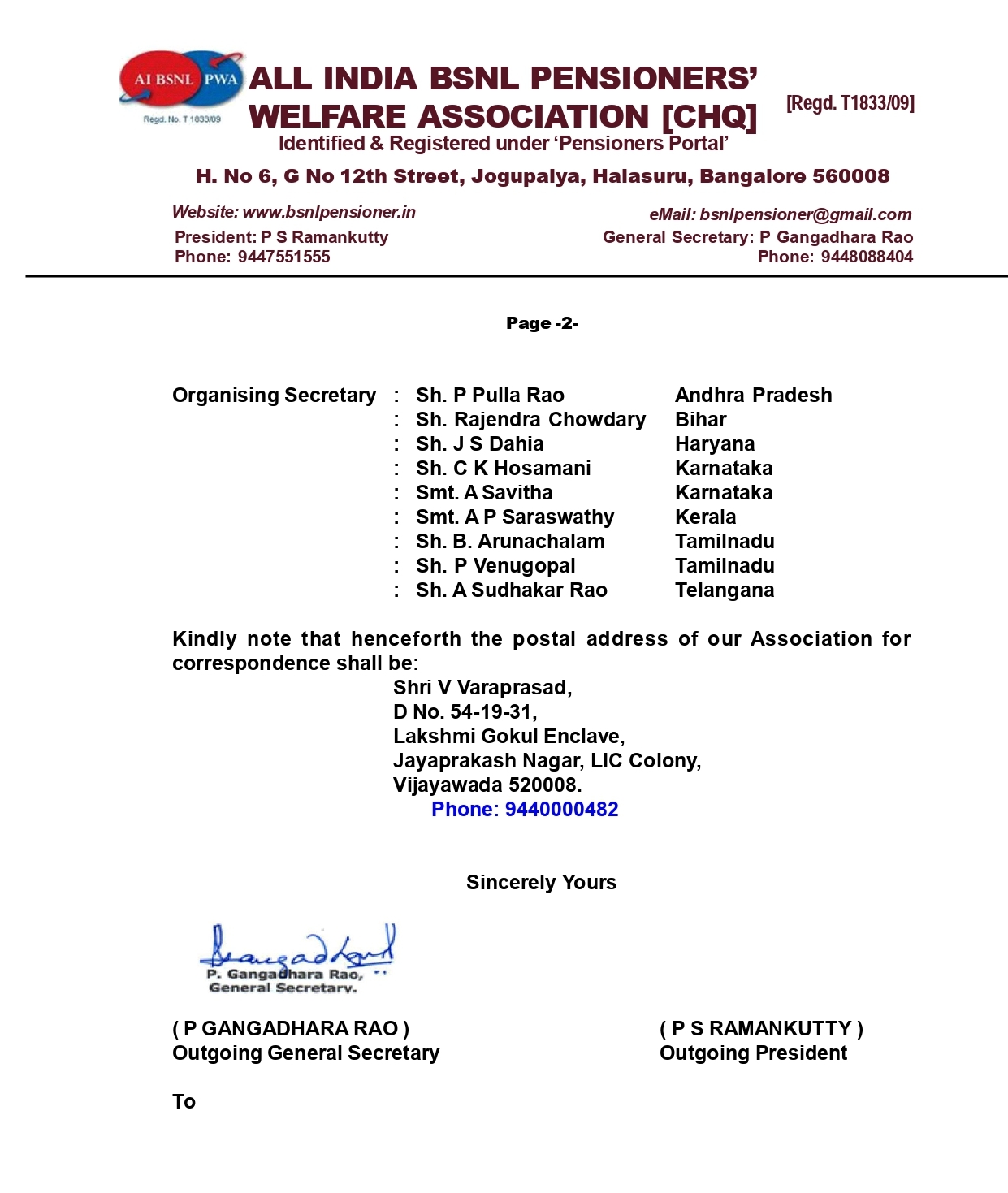

The elections are unanimous and the following are elected :

President : K S Koteswara Rao, Guntur

Circle Secretary : D Venkateswara Rao , Srikakulam

Treasurer : J Narayanachari, Vijayawada

With the help of Shri N K Gandigwad (OS, Hubli Branch), our resident Com. DG, our VP Com. Gangadhara Rao and myself along with Com. M K Bagchi (President, RTOWA), met Hon’ble Parliamentary Affairs Minister Shri Pralhad Joshiji in Parliament House on 13-12-2022 and requested his help to resolve the Pension Revision issue. Accordingly his PA fixed the meeting with MoC at 1900 hours.

MEETING WITH MOC

We met Hon’ble MoC Shri Ashwini Vaishnawji and handed over to him a letter containing our demand. We thanked him for taking a decision to delink Pension Revision from Pay Revision. We explained the justification for our demand and requested his intervention for 7th CPC fitment factor. He assured that he will get it examined.

MEETING WITH MEMBER (S) ON 14-12-2022.

we met Member (S). He told that Estt Section has asked from CGCA the

financial implications for 0%, 5%, 10% and 15%. He also told that though BSNL

could not reach an agreement on pay revision they have sent pay scales for

Non-executives. Then we told him about our meeting with Hon’ble MoC and handed

over a copy of the letter. He assured due consideration.

MEETING

WITH DDG (Estt)

We met

DDG (Estt) and discussed the following issues:

1.Pension

revision: She also told that they have asked for financial implications. We

told her that DoT has not sent the proposal of 2.515

2)

Implementation of Madras CAT judgement on extra increment to about 600 Pensioners

in Tamilnadu.

3)

Reduction of last pay drawn to Telecom Mechanics who were placed in LM scale

who did not get posting immediately after training due to want of vacancies in

Phone Mechanic cadre pertaining to Tamilnadu, Chennai

IT

NOTICES

We met

Director (Accounts) regarding IT notices being received by our members for Leave

Encashment of DOT period. On his request we supplied all correspondence we had with

Secretary of Revenue Department, MOF

V Vara Prasad, GS

Though our case was listed under item Bo 41 since our senior counsel mentioned , it came up for hearing today. Government Lawyer was also present.

Our senior counsel placed a few points before the Division Bench and the judges directed both the parties to submit a synopsis and it will further be heard on 6-2-2023

Please click here to read the two Resolutions adopted by Visakhapatnam AIC